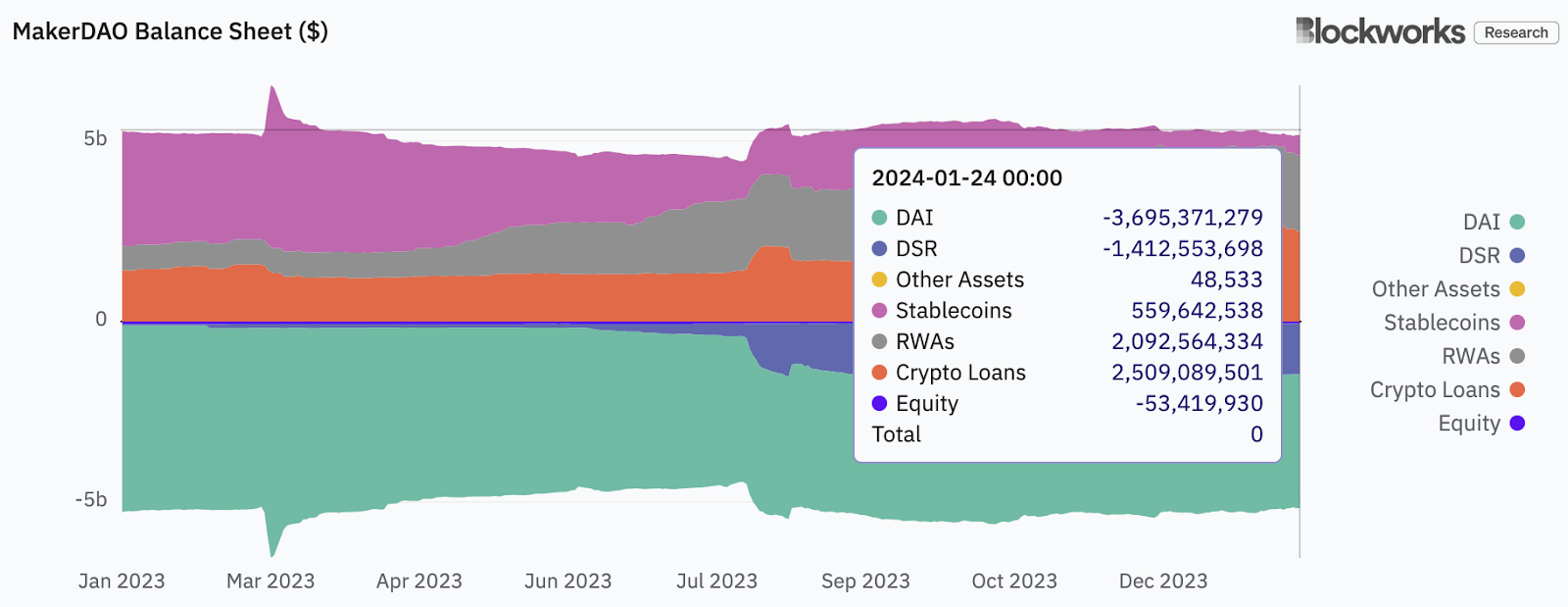

MakerDAO, issuer of the DAI stablecoin, has seen a notable shift in the composition of its balance sheet as a result of the combination of macroeconomic events and surging crypto markets.

The latest data from the DAO’s Digital Asset-Liability Committee (ALCO) shows that crypto-backed loans — that is, DAI issued against crypto collateral like ether — once again represent more than 50% of total assets, for the first time since May 2022.

For most of 2023, Maker’s public credit portfolio — think US T-bills — dominated the protocol’s revenue, as Federal Reserve rate hikes pushed interest rates on short term Treasurys above 5%.

But as yields fell in the fourth quarter of the year and demand for DAI borrowing picked up, the DAO, through its Special Purpose Vehicle (SPV) intermediaries began to sell off T-bills, according to Sebastian Derivaux at Steakhouse Financial, which advises the DAO.

“The reason we are decreasing T-bill exposure to replenish the [Peg Stability Module] and the reason why the PSM is shrinking lately is because we are in a bull market,” Derivaux told Blockworks. “And so as you can see, the crypto bank loans are going up a lot because people want to be speculating, and every time someone takes a loan [from] MakerDAO to get leverage, it decreases the PSM by the same amount, more or less.”

Read more: MakerDAO may expand non-crypto asset portfolio with BlockTower, Centrifuge

The ALCO flagged one item of mild concern related to the availability of stablecoins in Maker’s PSM in the minutes from its most recent meeting, published Wednesday.

“Daily liquidity has been consistently a bit short over the past few months,” the committee wrote. “The Digital ALCO recommends a medium-term priority to shift liquidity back a bit.”

The DAO has a target to have at least 18% to 22% of stablecoins available for the PSM, according to Derivaux.

“So sometimes it goes a bit down and then something is done to replenish the PSM,” he said.

Lately, the ratio of stablecoins to total assets has been running closer to 10%-12% according to Blockworks Research data.

ALCO discussed diversifying the protocol’s balance sheet further, specifically examining the suitability of Collateralized Loan Obligations (CLOs) and other asset classes as potential additions to seek higher yield than T-bills.

The committee acknowledged that it may be necessary to extend the duration of investments slightly, while being mindful of the risk associated with a potential return to a low interest rate macro environment down the road. CLOs typically have variable rates.

Read more: MakerDAO moves $250M from Coinbase to rebuild DAI collateral

For assets paying higher than T-bills, the committee considered senior tranches of Asset Backed Securities (ABS), especially those underpinned by floating assets like credit card receivables as well as short-term ETF bond funds.

These may juice returns while leaking risk low, but with tradeoffs, as well as potential challenges integrating these assets into Maker’s algorithmic Asset-Liability Management (ALM) scheme.

The ALCO recently added traditional finance heavyweight Moorad Choudhry as an independent advisor.

Steakhouse has based elements of its ALM research and proposals on Choudhry’s work in academia as a professor in the Department of Economics at London Metropolitan University and author of textbooks and references on finance.

While the ALCO concluded that holding additional asset types could help grow the balance sheet by increasing the Dai Savings Rate (DSR) — which is currently at 5% — it emphasized the need for careful consideration of capital adequacy, liquidity, price transparency and risk management integration.

Read more: DAI Savings Rate is at 8%, just not for Americans

A high percentage of the DAI that has been minted is not being staked for the 5% yield. Derivaux said that as much as 70% is just sitting in Externally Owned Accounts (EOAs) on Ethereum or layer-2 chains.

“That’s quite shocking because sDAI — maybe it’s not known by people — but it’s completely riskless,” he said, referring to the risk relative to holding unstaked DAI, which yields nothing.

The 5% rate should be sustainable, Derivaux said, as the balance sheet composition shifts. Demand for leverage should make collateral backed loans more profitable for the protocol.

“Obviously the less stablecoins we have [on the balance sheet], the more revenue MakerDAO is generating and the more profit it is generating,” he noted.